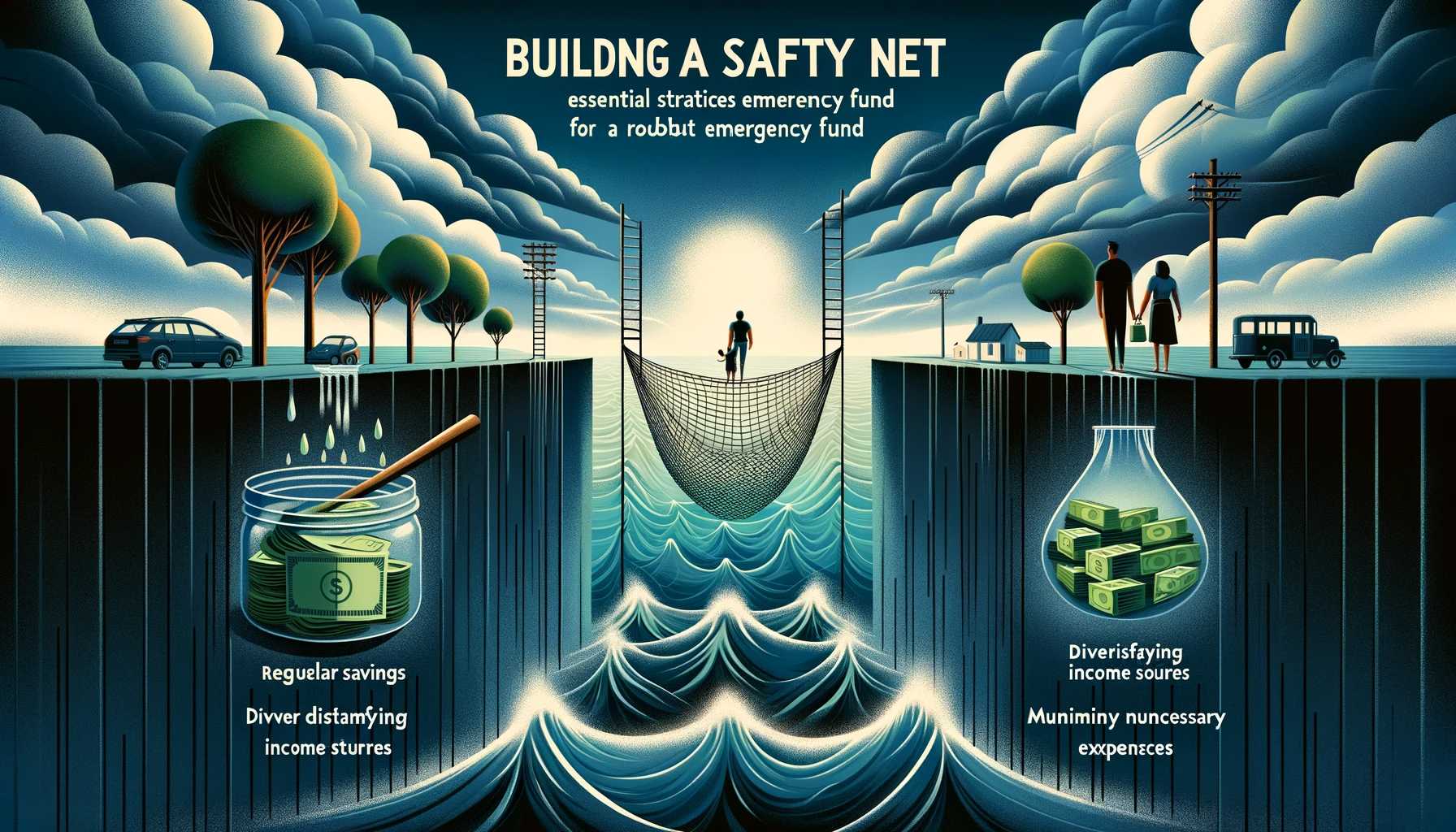

Building Your Safety Net: Essential Strategies for a Robust Emergency Fund

Life throws curveballs. Unexpected car repairs, medical bills, or job loss can disrupt even the most meticulously planned finances. An emergency fund acts as a crucial safety net, providing financial security during challenging times. This blog post dives into effective strategies for building and maintaining a robust emergency fund, empowering you to weather financial storms with confidence.

Why is an Emergency Fund Important?

Imagine facing a sudden car breakdown or a medical emergency without the financial resources to address it. This is where an emergency fund comes to the rescue. It provides the necessary funds to cover unexpected expenses without resorting to high-interest debt, selling assets at a loss, or jeopardizing your long-term financial goals.

Determining the Ideal Emergency Fund Size:

The ideal emergency fund size varies depending on your individual circumstances. Factors to consider include:

- Your income and living expenses: Aim for an emergency fund that covers 3-6 months of essential living expenses. This provides a buffer to navigate unexpected financial disruptions without significant hardship.

- Your dependents: If you have dependents, consider increasing your emergency fund to cover their essential needs as well.

- Job security: If your job security is uncertain, consider building a larger emergency fund to provide a safety net for potential job loss.

- Debt obligations: Existing debt can increase your financial vulnerability. Aim for a larger emergency fund if you have significant debt obligations.

Strategies for Building Your Emergency Fund:

1. Automate Your Savings:

Set up automatic transfers from your checking account to your emergency savings account. This ensures consistent contributions and removes the temptation to spend the money. Start with a small, manageable amount and gradually increase it as your financial situation allows.

2. Utilize Windfalls:

Treat unexpected income, such as tax refunds or bonuses, as opportunities to boost your emergency fund. Allocate a portion of these windfalls towards your emergency savings instead of using them for discretionary spending.

3. Review Your Budget and Cut Back:

Analyze your budget and identify areas where you can reduce unnecessary expenses. Even small cuts can add up significantly over time. Allocate the saved funds towards your emergency fund.

4. Explore Alternative Income Streams:

Consider generating additional income through side hustles, freelance work, or selling unused items. Channel these earnings towards building your emergency fund.

5. Leverage Savings Challenges:

Participate in savings challenges, such as the 52-week challenge, where you save a specific amount each week for a year. This gamifies the saving process and helps you accumulate funds gradually.

Choosing the Right Savings Account for Your Emergency Fund:

While any savings account is better than none, consider these factors when choosing an account for your emergency fund:

- Liquidity: Opt for an account with easy access to your funds, allowing you to withdraw them quickly when needed.

- Security: Choose an account with FDIC (Federal Deposit Insurance Corporation) or NCUA (National Credit Union Administration) insurance to protect your deposits up to a certain limit.

- Interest Rate: While not the most crucial factor, consider accounts offering a competitive interest rate to help your emergency fund grow slightly over time.

Maintaining and Replenishing Your Emergency Fund:

Building an emergency fund is just the first step. Regularly review your emergency fund size and adjust it based on changes in your income, expenses, or life circumstances. Replenish your emergency fund after using it to address unexpected expenses. Remember, your emergency fund is not meant to be a permanent solution but a temporary safety net during challenging times.

Additional Tips for a Robust Emergency Fund:

- Communicate with your family: Discuss the importance of the emergency fund with your family members and involve them in the saving process.

- Review your insurance coverage: Ensure you have adequate health, auto, and homeowner's insurance to minimize the financial impact of unexpected events.

- Seek professional guidance: If you struggle to build or manage your emergency fund, consider consulting a financial advisor for personalized advice.

Beyond the Basics: Advanced Strategies for a Bulletproof Emergency Fund

While the core principles of building and maintaining an emergency fund remain crucial, there are additional strategies you can explore to further solidify your financial safety net. This section delves into advanced techniques for those seeking to optimize their emergency fund strategy:

1. Utilize Multiple Savings Accounts:

Diversify your emergency fund by allocating portions to different accounts with varying liquidity and interest rates. Consider a high-yield savings account for a readily accessible portion and a certificate of deposit (CD) for a longer-term, less accessible portion that earns a higher interest rate.

2. Leverage Tax-Advantaged Accounts:

Explore tax-advantaged accounts like Health Savings Accounts (HSAs) or employer-sponsored emergency savings accounts, if available. These accounts offer tax benefits on contributions and potentially earnings, further boosting your emergency fund growth.

3. Consider Emergency Fund Insurance:

Specific insurance products, such as critical illness insurance or disability income insurance, can act as a safety net in case of unforeseen medical conditions or job loss. Evaluate your needs and risk tolerance before opting for such insurance products.

4. Build a "Second Line of Defense":

While an emergency fund should ideally cover unexpected expenses, consider building a "second line of defense" for larger, infrequent events like major home repairs or car replacements. This could involve saving towards specific goals in separate accounts or exploring lines of credit with low-interest rates for planned emergencies.

5. Regularly Review and Adapt:

As your life circumstances evolve, your emergency fund needs may change. Regularly review your emergency fund size, consider factors like potential career changes, family additions, or increased living expenses, and adjust your savings goals and strategies accordingly.

Remember:

- Balance is key: While building a robust emergency fund is essential, avoid neglecting other financial goals like retirement savings or debt repayment. Maintain a healthy balance between your emergency fund and other financial priorities.

- Emergency preparedness goes beyond finance: Consider non-financial aspects of emergency preparedness, such as having a disaster plan, building a home emergency kit, and ensuring proper insurance coverage for your belongings.

- Seek professional guidance: If you require personalized advice or have complex financial situations, consulting a financial advisor can help you develop a comprehensive emergency fund strategy tailored to your unique needs.

Conclusion:

Building a robust emergency fund is an essential step towards achieving financial security and peace of mind. By implementing these strategies and prioritizing your emergency savings, you can prepare yourself to face unexpected challenges with confidence and navigate life's uncertainties with greater financial resilience. Remember, financial well-being is a journey, and building a strong emergency fund is a crucial step on the path towards a secure and fulfilling future.